Individuals purchasing coverage through the Affordable Care Act’s (ACA) health insurance marketplaces may have difficulty finding consistent, clear information on whether a plan includes or excludes abortion coverage. However, transparency about abortion coverage is both necessary and achievable, according to a new analysis published in the Guttmacher Policy Review.

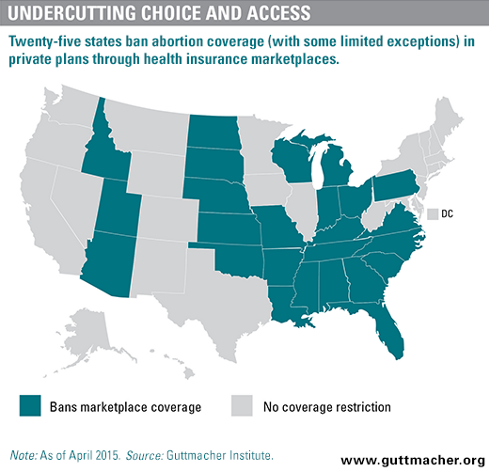

Under the ACA, insurance plans are neither required to nor prohibited from covering abortion. However, 25 states prohibit coverage of abortion on their health insurance marketplaces. In the remaining states and the District of Columbia, issuers can offer plans that cover abortion care beyond the narrow instances of rape, incest or when the woman’s life is endangered. But a new Guttmacher analysis of publicly available 2015 plan documents in these states found the vast majority of plans do not include information on whether and to what extent abortion is covered. Among the minority of issuers that do address abortion coverage, the way the information is provided varies considerably and is not always useful.

"The lack of transparency is problematic for individuals trying to make an informed decision about their coverage," says Kinsey Hasstedt, author of the new analysis. "But there is a political dimension, as well. Policymakers and activists who oppose abortion rights have exploited this issue and seized the opening it has created to advance their main agenda: to ban virtually all private and public insurance coverage of abortion."

In December, the Obama administration proposed new regulations—still being finalized in response to public comments—to provide greater clarity in plans’ abortion coverage. Among other steps, these proposed rules would require issuers offering plans on ACA marketplaces to state clearly whether abortion care is covered or excluded. Hasstedt argues that while this effort goes in the right direction, additional steps are needed. The recommendations detailed in the analysis include the following:

- Issuers should be required to post an electronic summary of benefits and coverage (SBC) for each plan offered through each insurance marketplace website. SBCs should also be posted to insurers’ own websites.

- All plans—not just marketplace plans—should be required to provide information on abortion coverage and exclusions, including in states where abortion coverage is banned in the ACA marketplace.

- Issuers should be given specific guidance to include information on abortion coverage in the same place on each SBC, using consistent, accessible and neutral language.

- All SBCs should include a link to detailed plan documents and thorough explanations of the coverage or exclusion of abortion, among other health services.

Hasstedt further argues that, beyond transparency, all U.S. women should have at least one plan option that includes abortion services, something that is not the case in most states today. The Obama administration could address this shortcoming, at least in states where abortion coverage is permissible, by ensuring the availability of at least one plan that covers abortion care. However, even this would leave abortion coverage unattainable for women in states that ban such coverage.

"The bottom line is that abortion is basic health care and should be covered by insurance accordingly," says Hasstedt. "However, few people buying insurance base their entire decision on whether the plan covers an individual service—particularly a service like abortion, which no woman plans to need. Given these realities, what women really need is the option to use their health coverage for abortion if and when they find themselves in need of such care. Unfortunately, policymakers have taken that decision out of far too many women’s hands."